Table of Contents

4

Recording of Transactions-II

Learning Objectives

After studying this chapter, you will be able to :

• state the need for special purpose books;

• record the transactions in cash book and post them in the ledger;

• prepare the petty cash book;

• record the transactions in the special purpose books;

• post the entries in the special purpose book and to the ledger;

• balance the ledger accounts.

In chapter 3, you learnt that all the business transactions are first recorded in the journal and then they are posted in the ledger accounts. A small business may be able to record all its transactions in one book only, i.e., the journal. But as the business expands and the number of transactions becomes large, it may become cumbersome to jour-nalise each transaction. For quick, efficient and accurate recording of business transactions, Journal is sub-divided into special journals. Many of the business transactions are repetitive in nature. They can be easily recorded in special journals, each meant for recording all the transactions of a similar nature. For example, all cash transactions may be recorded in one book, all credit sales transactions in another book and all credit purchases transactions in yet another book and so on. These special journals are also called daybooks or subsidiary books. Transactions that cannot be recorded in any special journal are recorded in journal called the Journal Proper. Special journals prove economical and make division of labour possible in accounting work. In this chapter we will discuss the following special purpose books:

• Cash Book

• Purchases Book

• Purchases Return (Return Outwards) Book

• Sales Book

• Sales Return (Return Inwards) Book

• Journal Proper

4.1 Cash Book

Cash book is a book in which all transactions relating to cash receipts and cash payments are recorded. It starts with the cash or bank balances at the beginning of the period. Generally, it is made on monthly basis. This is a very popular book and is maintained by all organisations, big or small, profit or not-for-profit. It serves the purpose of both journal as well as the ledger (cash) account. It is also called the book of original entry. When a cashbook is maintained, transactions of cash are not recorded in the journal, and no separate account for cash or bank is required in the ledger.

4.1.1 Single Column Cash Book

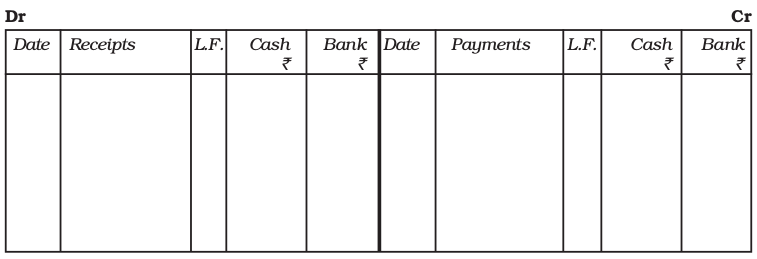

The single column cash book records all cash transactions of the business in a chronological order, i.e., it is a complete record of cash receipts and cash payments. When all receipts and payments are made in cash by a business organisation only, the cash book contains only one amount column on each (debit and credit) side. The format of single column cash book is shown in figure 4.1.

Cash Book

Cr.

Dr.

| Date | Receipts | L.F. | Amount Rs. | Date | Payments | L.F. | Amount Rs |

| F |

Fig. 4.1 : Format of single column cash book

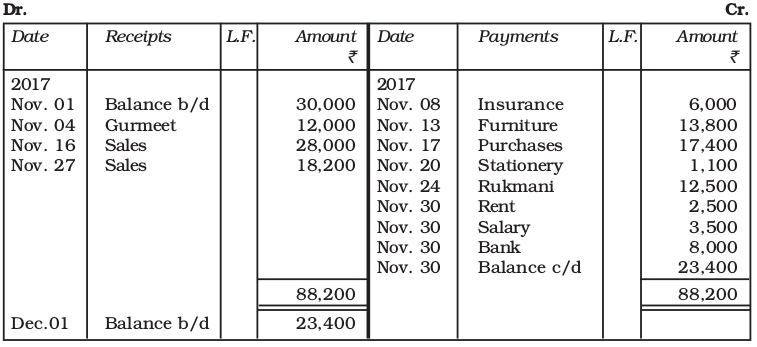

Recording of entries in the single column cash book and its balancing is illustrated by an example. Consider the following transactions of M/s Roopa Traders observe how they are recorded in a single column cash book.

| Date......... | Details | Amount Rs. |

2017 Nov. 01 Nov. 04 Nov. 08 Nov. 13 Nov. 16 Nov. 17 Nov. 20 Nov. 24 Nov. 27 Nov. 30 Nov. 30 Nov. 30 | Cash in hand Cash received from Gurmeet Insurance paid (Annual Instalment) Purchased furniture Sold goods for cash Purchased goods from Mudit in cash Purchase stationery Cash paid to Rukmani in full settlement of account Sold goods to Kamal for cash Paid monthly rent Paid salary Deposited in bank | 30,000 12,000 6,000 13,800 28,000 17,400 1,100 12,500 18,200 2,500 3,500 8,000 |

Roopa Traders

Cash Book

Posting of the Single Column Cash Book

As evident from figure 4.1, the left side of the cash book shows the receipts of the cash whereas the right side of the cash book shows all the payments made in cash. The accounts appearing on then debit side for the cash book are credited in the respective ledger accounts because cash has been received in respect of them. Thus, in our example, an entry ‘cash received from Gurmeet’ appears on the debit side of the cash book conveys that the cash has been received from Gurmeet. Therefore, in the ledger, Gurmeet’s account will be credited by writing ‘Cash’ in the particulars column on the credit side. Similarly, all the account names appearing on the credit side of the cash book are debited as cash/cheque has been paid in respect of them. Now, notice, how the transactions in our example are posted to the related ledger accounts:

Books of Roopa Traders

Gurmeet’s Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Nov.04 | Cash | 12,000 | |||||

Sales Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Nov.16 Nov.27 | Cash Cash | 28,000 18,200 | |||||

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Nov.18 | Cash | 6000 | |||||

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

2017 Nov. 13 | Cash | 13,800 | |||||

Purchases Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Nov.17 | Cash | 13,800 | |||||

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Nov.20 | cash | 1,100 | |||||

Rukmani’s Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Nov.30 | Cash | 2,500 | |||||

Rent Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Nov.30 | Cash | 2,500 | |||||

Salary Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Nov.30 | Cash | 3,500 | |||||

Bank’s Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Nov.30 | Cash | 8,000 | |||||

4.1.2 Double Column Cash Book

In this type of cash book, there are two columns of amount on each side of the cash book. In fact, now-a-days bank transactions are very large in number. In many organisations, as far as possible, all receipts and payments are affected through bank.

A businessman generally opens a current account with a bank. Bank, do not allow any interest on the balance in current account but charge a small amount, called incidental charges, for the services rendered.

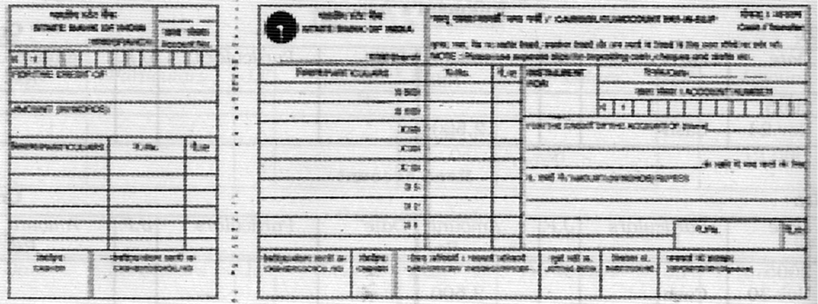

For depositing cash/cheques in the bank account, a form has to be filled, which is called a pay-in-slip. (refer figure 4.2) It contains a counterfoil also which is returned to the customer (depositor) with the signature of the cashier, as receipt.

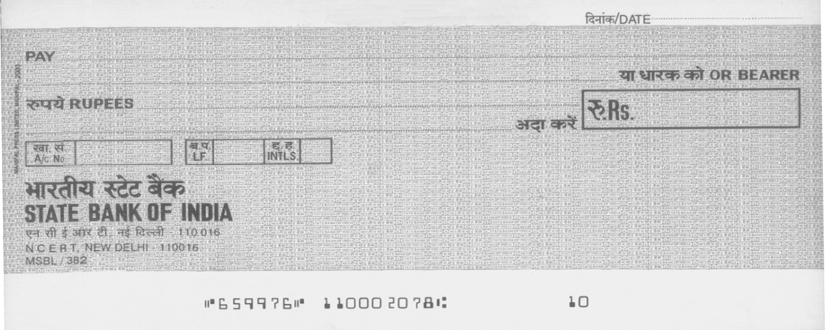

The bank issues blank cheque forms, to the account holder for withdrawing money. (refer figure 4.3) The depositor writes the name of the party to whom payment is to be made after the words Pay printed on the cheque. Cheque forms have the printed word bearer, which means payment is to be made to the person whose name has been written after the words “pay” or the bearer of the cheques. When the world ‘bearer’ is struck off by drawing a line, the cheque becomes an order cheque. It means payment is to be made to the person whose name is written on the cheque or to his order after proper identification.

Fig. 4.3 : A cheque

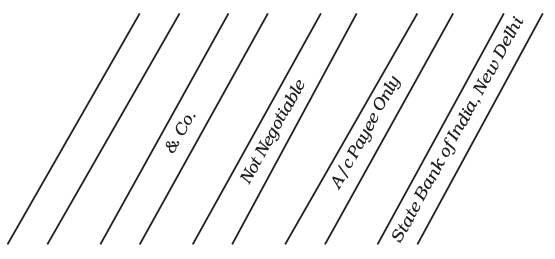

Cheques are generally crossed in practice. The payment of a crossed cheque cannot be made direct to the party on the counter. It is to be paid only through a bank. When two parallel lines are drawn across the cheque, it is said to be crossed. The various types of crossing providing different degrees of safety to the payment are shown in figure 4.4.

In case of an A/c payee only crossing, the amount of the cheque can be deposited only in the account of the person whose name appears on the cheque. When the name of the bank is written between two parallel lines, it becomes a special crossing and the payment can be made only to the bank whose name has been written between the two lines.

Though this is rarely done, a cheque can be transferred by the payee (the person in whose favour the cheque has been drawn) to another person, if it is not crossed A/c payee only. A bearer cheque can be passed on by mere delivery. An order cheque can be transferred by endorsement and delivery. Endorsement means the writing of instructions to pay the cheque to a particular person and then singing it on the back of the cheque.

Fig. 4.4 : Types of crossing

When the number of bank transactions is large; it is convenient to have a separate amount column for bank transactions in the cash book itself instead of recording them in the journal. This helps in getting information about the position of the bank account from time to time. Just like cash transactions, all payments into the bank are recorded on the left side and all withdrawals/payments through the bank are recorded on the right side. When cash is deposited in the bank or cash is withdrawn from the bank, both the entries are recorded in the cash book. This is so because both aspects of the transaction appear in the cash book itself. When cash is paid into the bank, the amount deposited is written on the left side in the bank column and at the same time the same amount is entered on the right side in the cash column. The reverse entries are recorded when cash is withdrawn from the bank for use in the office. Against such entries the word C, which stands for contra is written in the L.F. column indicating that these entries are not to be posted to the ledger account.

The bank column is balanced in the same way as the cash column. However, in the bank column, there can be credit balance also because of overdraft taken from the bank. Overdraft is a situation when cash withdrawn from the bank exceeds the amount of deposit. Entries in respect of cheques received should be made in the bank column of the cash book. When a cheque is received, it may be deposited into the bank on the same day or it may be deposited on another day. In case, it is deposited on the same day the amount is recorded in the bank column of the cash book on the receipts side. If the cheque is deposited on another day, in that case, on the date of receipt it is treated as cash received and hence recorded in the cash column on the receipts side. On the day of deposit to the bank, it is shown in the Bank Column on receipt (Dr.) side and in the Cash Column on the payment (Cr.) side. This is a contra entry.

If a cheque received from a customer is dishonoured, the bank will return the dishonoured cheque and debit the firm’s account. On receipt of such cheque or intimation from the bank, the firm will make an entry on the credit side of the cash book by entering the amount of the dishonoured cheque in the bank column and the name of the customer in the particulars column. This entry will restore the position prevailing before the receipt of the cheque form the customer and its deposit in the bank. Dishonour of a cheque means return of the cheque unpaid, generally due to insufficient funds in the customer’s account with the bank.

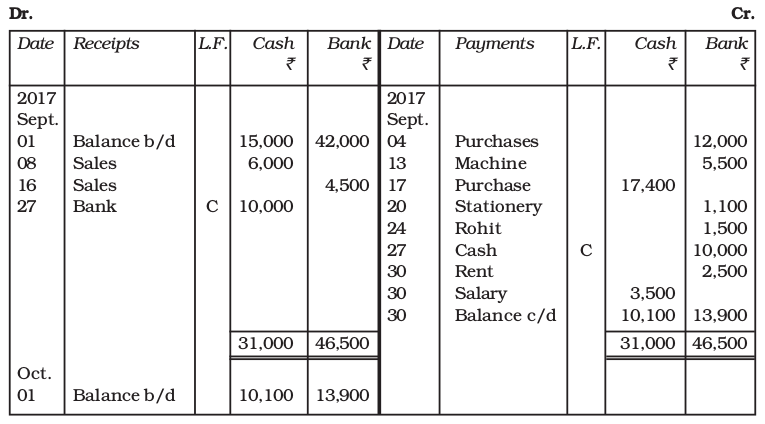

If the bank debits the firm on account of interest, commission or other charges for bank services, the entry will be made on the credit side in bank column. If the bank credits the firm’s account, the entry will be made on the debit side of the cash book in the appropriate column. The format of double column cash book is shown in figure 4.5.

Cash Book

Fig. 4.5 : Format of a double column cashbook

We will now learn how the transactions are recorded in the double column cash book.

Consider the following example:

The following transactions related to M/s Tools India :

Date Details Amount ₹

2017

Sept. 01 Bank balance 42,000

Sept. 01 Cash balance 15,000

Sept. 04 Purchased goods by cheque 12,000

Sept. 08 Sales of goods for cash 6,000

Sept. 13 Purchased machinery by cheque 5,500

Sept. 16 Sold goods and received cheque (deposited same day) 4,500

Sept. 17 Purchase goods from Mriaula in cash 17,400

Sept. 20 Purchase stationery by cheque 1,100

Sept. 24 Cheque given to Rohit 1,500

Sept. 27 Cash withdrawn from bank 10,000

Sept. 30 Rent paid by cheque 2,500

Sept. 30 Paid salary 3,500

The double column cash book based upon above business transactions will prepared as follows :

When the bank column is maintained in the cash book, the bank account also is not opened in the ledger. The bank column serves the purpose of the bank account. Entries marked C (being contra entries as explained earlier) are ignored while posting from the cash book to the ledger. These entries represent debit or credit of cash account against the bank account or vice-versa. We will now see how the transactions recorded in double column cash book are posted to the individual accounts.

Purchases Account

| Receipts | Payments | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Sept.04 Sept.17 | Cash Bank | 12,000 17,400 | |||||

Sales Account

| Receipts | Payments | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Sept.04 Sept.17 | Cash Bank | 6,000 4,500 | |||||

Machinery Account

| Receipts | Payments | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Sept.13 | Cash Bank | 12,000 17,400 | |||||

Stationery Account

| Receipts | Payments | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Sept.20 | Bank | 1,100 | |||||

Rohit’s Account

| Receipts | Payments | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Sept.20 | Bank | 1,500 | |||||

Rent Account

| Receipts | Payments | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Sept.20 | Bank | 2,500 | |||||

Salary Account

| Receipts | Payments | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Sept.20 | Bank | 3,500 | |||||

4.1.3 Petty Cash Book

In every organisation, a large number of small payments such as conveyance, cartage, postage, telegrams and other expenses (collectively recorded under miscellaneous expenses) are made. These are generally repetitive in nature. If all these payments are handled by the cashier and are recorded in the main cash book, the procedure is found to be very cumbersome. The cashier may be overburdened and the cash book may become very bulky. To avoid this, large organisations normally appoint one more cashier (petty cashier) and maintain a separate cash book to record these transactions. Such a cash book maintained by petty cashier is called petty cash book.

The petty cashier works on the Imprest system. Under this system, a definite sum, say ` 2,000 is given to the petty cashier at the beginning of a certain period. This amount is called imprest amount. The petty cashier goes on making all small payments out of this imprest amount and when he has spent the substantial portion of the imprest amount say `1,780, he gets reimbursement of the amount spent from the head cashier. Thus, he again has the full imprest amount in the beginning of the next period. The reimbursement may be made on a weekly, fortnightly or monthly basis, depending on the frequency of small payments. (In certain cases, the petty cash system is operated through the main cash book itself. In such instances, the petty cash book is not maintained independently.)

The petty cash book generally has a number of columns for the amount on the payment side (credit) besides the first other amount column. Each of the amount columns is allotted for items of specific payments, which are most common. The last amount column is designated as ‘Miscellaneous’ followed by a ‘Remarks’ column. In the miscellaneous column those payments are recorded for which a separate column does not exist. In the ‘Remarks’ the nature of payment is recorded. At the end of the period, all amount columns are totaled. The total amount column l shows the total amount spent and to be reimbursed. On the receipt (debit) side, there is only one amount column. Columns for the date, voucher number and particulars are common for both receipts and payments.

Box 1

Advantages of Maintaining Petty Cash Book

1. Saving of Time and efforts of chief cashier: The chief cashier is not required to deal with petty disbursements. He can concentrate on cash transactions involving large amount of cash. It saves time and labour and helps chief cashier to discharge his duties more effectively

2. Effective control over cash disbursements: Cash control becomes easy because of division of work. The head cashier can control big payments directly and petty payments by keeping a proper check on the petty cashier. This way the chances of making frauds and embezzlements become very difficult.

3. Convenient recording: Recording of petty disbursements in the main cash book makes it bulky and unmanageable. Further, the materiality principle requires that insignificant details need not be given in the main cashbook. This way the cash book reveals only material and useful information.

Recording of such small payments becomes easy as the totals of different types of expenses are posted to ledger. It also saves time and effort of posting individual items in the ledger. In nutshell it can be stated that preparation of petty cash book is a cost reduction control measure.

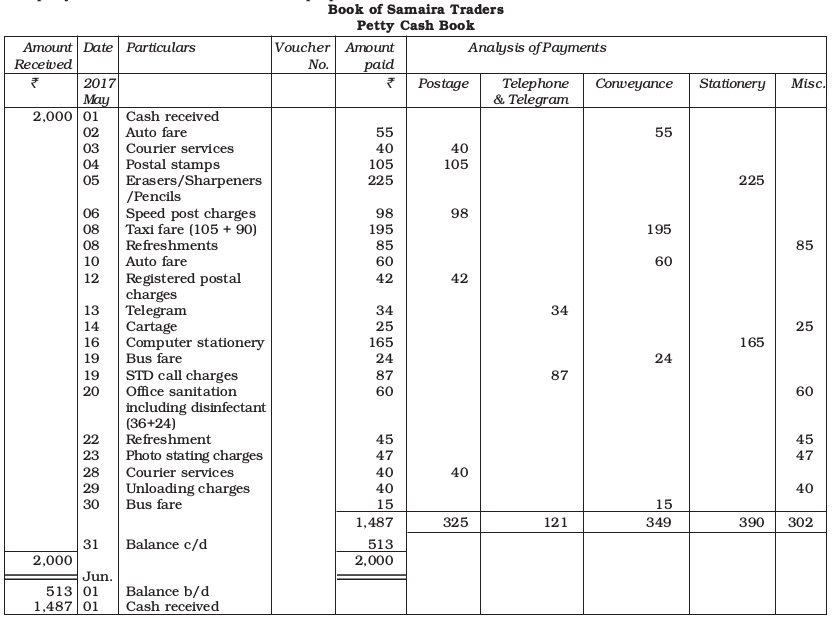

For example, Mr. Mohit, the petty cahier of M/s Samaira Traders received Rupees 2,000 on May 01, 2017 from the Head Cashier. For the month, details of petty expenses are listed here under:

| Date | Details | Amount Rs |

| 2017 | ||

| May | ||

02 03 04 05 06 08 08 10 12 13 14 16 19 19 20 22 23 28 29 30 | Auto fare Courier services Postal stamps Erasers/Sharpeners/Pencils/Pads Speed post charges Taxi fare (105 + 90) Refreshments Auto fare Registered postal charges Telegram Cartage Computer stationery Bus fare STD call charges Office sanitation including disinfectant (₹ 36 + ₹ 24) Refreshment Photo stating charges Courier services Unloading charges Bus fare | 55 40 105 225 98 195 85 60 42 34 25 165 24 87 60 45 47 40 40 15 |

Posting from the Petty Cash Book

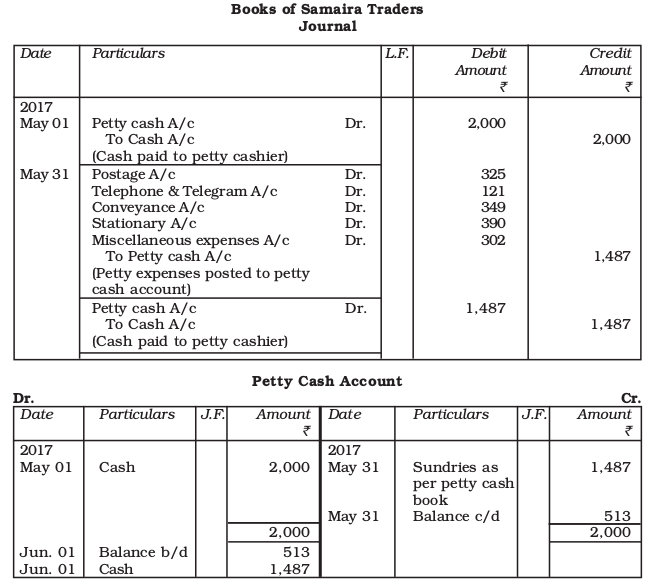

The petty cash book is balanced periodically. The difference between the total receipts and total payments is the balance with the petty cashier. The balance is carried to the next period and the petty cashier is paid the amount actually spent. A petty cash account is opened in the ledger. It is debited with the amount given to petty cashier. Each expense account is individually debited with the periodic total as per the respective column by writing “petty cash account” and the petty cash account is credited with the total expenditure incurred during the period by writing sundries as per petty cash book. The petty cash account is balanced. It reflect the actual cash with the petty cashier.

The petty cash book for the month will be prepared as follows :

Books of Samaria Traders

Postage Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 May.31 | Petty cash | 325 | |||||

Telephone and Telegram Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 May.31 | Petty cash | 121 | |||||

Conveyance Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 May.31 | Petty cash | 349 | |||||

Stationery Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 May.31 | Petty cash | 390 | |||||

Miscellaneous Expenses Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 May.31 | Petty cash | 302 | |||||

4.1.4 Balancing of Cash Book

On the left side, all cash transactions relating to cash receipts (debits) and on the right side all transactions relating to cash payments (credits) are entered date-wise. When a cash book is maintained, a separate cash book in the ledger is not opened. The cash book is balanced in the same way as an account in the ledger. But it may be noted that in the case of the cash book, there will always be debit balance because cash payments can never exceed cash receipts and cash in hand at the beginning of the period.

The source document for cash receipts is generally the duplicate copy of the receipt issued by the cashier. For payment, any document, invoice, bill, receipt, etc., on the basis of which payment has been made, will serve as a source document for recording transactions in the cash book. When payment has been made, all these documents, popularly known as vouchers, are given a serial number and filed in a separate file for future reference and verification.

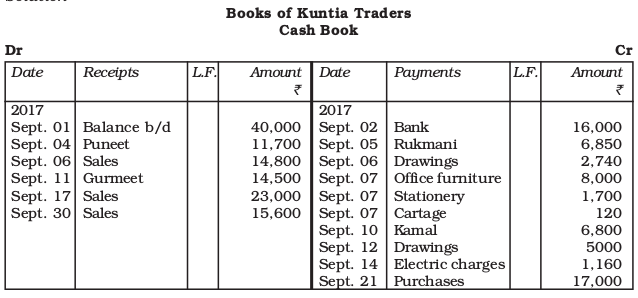

Illustration 1

From the following transactions made by M/s Kuntia Traders, prepare the single column cashbook.

| Date....... | Details | Amount Rs. |

| 2017 Sept. 01 Sept. 02 Sept. 04 Sept. 05 Sept. 06 Sept. 06 Sept. 07 Sept. 07 Sept. 07 Sept. 10 Sept. 11 Sept. 12 Sept. 14 Sept. 17 Sept. 21 Sept. 24 Sept. 26 Sept. 28 Sept. 29 Sept. 29 Sept. 30 | Cash in hand Deposited in bank Received from Puneet in full settlement of claim of 12,000. Cash paid to Rukmani in full settlement of claim of 7,000 Sold goods to Sudhir for cash Paid quarterly insurance premium on policy for proprietor’s wife Purchased office furniture Purchased stationery Paid cartage Paid Kamal, discount allowed by him 200 Received from Gurmeet, discount allowed to him 500 Amount withdrawn for house hold use Electricity bill paid Goods sold for cash Bought goods from Kamal on cash basis Paid telephone charges Paid postal charges Paid monthly rent Paid monthly wages and salary Bought goods for cash Sold goods for cash | 40,000 16,000 11,700 6,850 14,800 2,740 8,000 1,700 120 6,800 14,500 5,000 1,160 23,000 17,000 2,300 520 4,200 8,250 11,000 15,600 |

Illustration 2

Record the following transactions in double column cash book and balance it.

Solution

Cash Book

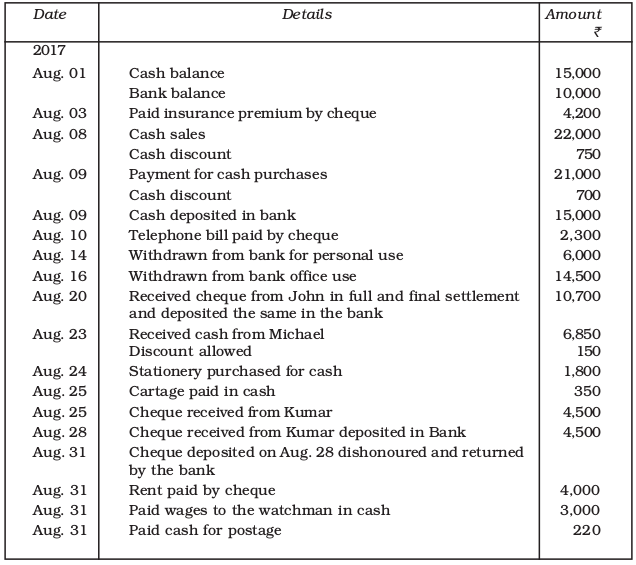

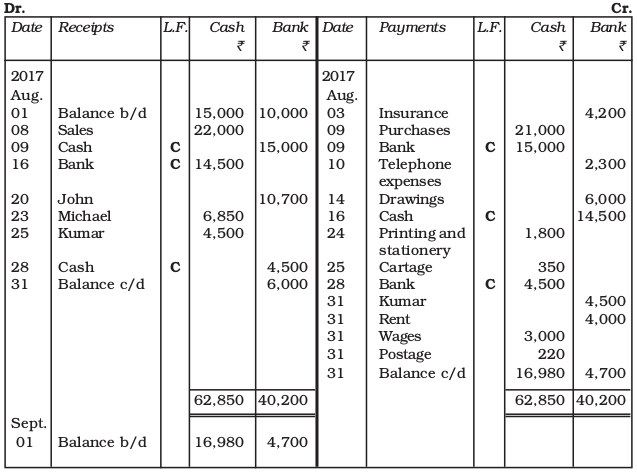

Illustration 3

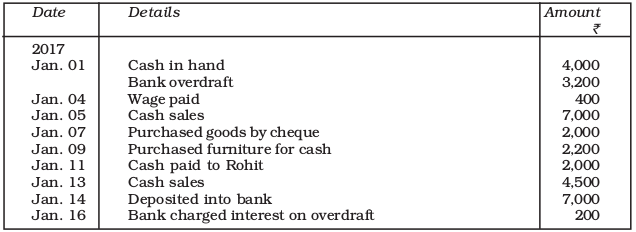

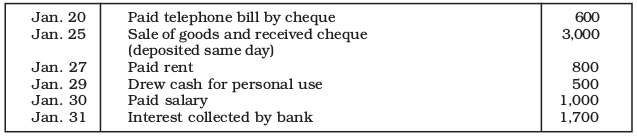

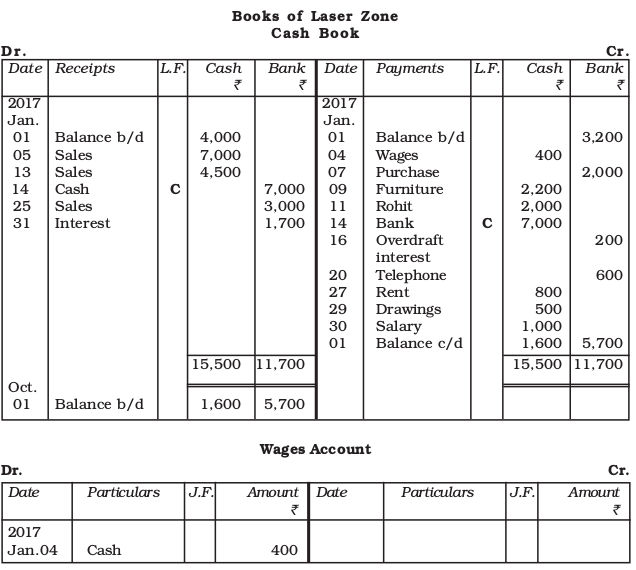

Prepare bank column cash book from the following tansactions of M/s Laser Zone for the

month of January 2014 and post them to the related ledger accounts :

Solution

Wages Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Jan.04 | Cash | 400 | |||||

Sales Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Jan,05 Jan.13 Jan.25 | Cash Cash Bank | 7,000 4,500 3,000 | |||||

Purchases Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Jan.07 | Bank | 2,000 | |||||

Furniture Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Jan.09 | Cash | 2,200 | |||||

Rohit Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Jan.11 | Cash | 2000 | |||||

Ovedraft Interest (Paid) Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Jan.16 | Cash | 200 | |||||

Telephone Expenses Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Jan.16 | Bank | 600 | |||||

Rent Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Jan.27 | Cash | 800 | |||||

Drawings Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Jan.29 | Cash | 500 | |||||

Salary Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Jan.30 | Cash | 1,000 | |||||

Interest (Received) Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2017 Jan.31 | Bank | 1,700 | |||||

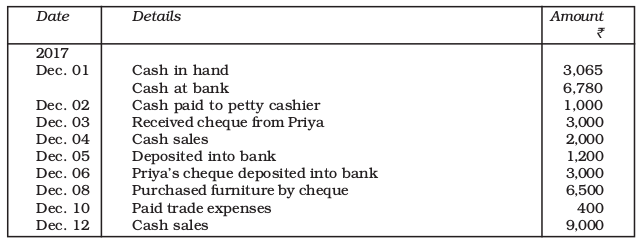

Illustration 4

Prepare double column cash book of M/s Advance Technology Pvt. Ltd. for the month of

December 2014 from the following transactions :

Solution

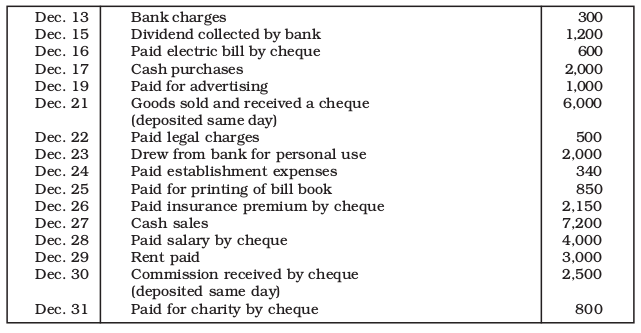

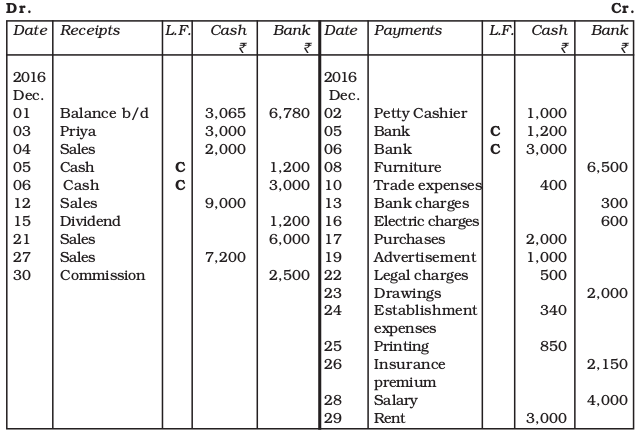

Books of Advance Technology

Cash Book

Petty Cashier’s Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.02 | Cash | 1,000 | |||||

Priya’s Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.03 | Cash | 3,000 | |||||

Sales Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.04 Dec.12 Dec.21 Dec.27 | Cash Cash Bank Cash | 2,000 9,000 6,000 7,200 | |||||

Furniture Account

| Date | Particulars | J.F. | Amount Rs. | Date | Particulars | J.F. | Amount Rs |

| 2016 | Bank | 6,500 |

Trade Expenses Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.10 | Cash | 400 | |||||

Bank Charges Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.13 | Bank | 300 | |||||

Dividend Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.03 | Bank | 1,200 | |||||

Electric Charges Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.16 | Cash | 600 | |||||

Purchases Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.17 | Cash | 2,000 | |||||

Advertisement Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.19 | Cash | 1,000 | |||||

Legal Charges Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.22 | Cash | 500 | |||||

Drawings Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.23 | Bank | 2,000 | |||||

Establishment Expenses Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.24 | Cash | 340 | |||||

Printing Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.25 | Cash | 850 | |||||

Insurance Premium Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.26 | Bank | 2,150 | |||||

Salary Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.28 | Bank | 4,000 | |||||

Rent Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.29 | Cash | 3,000 | |||||

Commission Received Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.30 | Bank | 2,500 | |||||

Charity Account

| Dr. | Cr. | ||||||

| Date | Particulars | J.F. | Amount ₹ | Date | Particulars | J.F. | Amount ₹ |

| 2016 Dec.31 | Bank | 800 | |||||

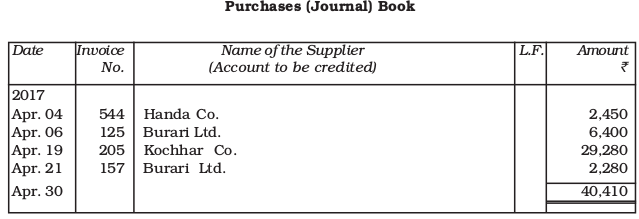

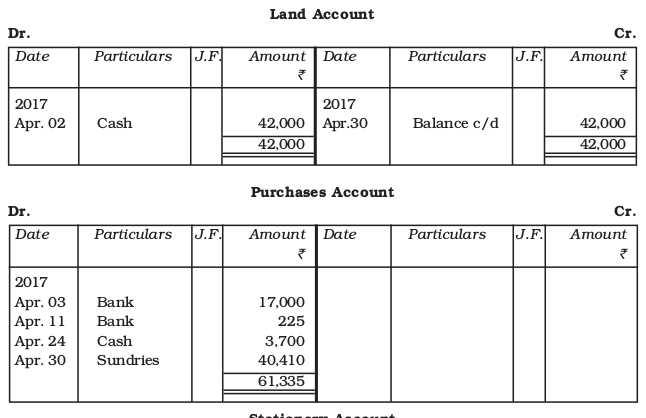

4.2 Purchases (Journal) Book

All credit purchases of goods are recorded in the purchases journal whereas cash purchases are recorded in the cash book. Other purchases such as purchases of office equipment, furniture, building, are recoded in the journal proper if purchased on credit or in the cash book if purchased for cash. The source documents for recording entries in the book are invoices or bills received by the firm from the supplies of the goods. Entries are made with the net amount of the invoice. Trade discount and other details of the invoice need not be recorded in this book. The format of the purchases journal is shown in figure 4.6.

Purchases (Journal) Book

| Date | Invoice No. | Name of Supplier (Account to be credited) | L.F. | Amount Rs. |

Fig. 4.6 : Format of purchases (journal) book

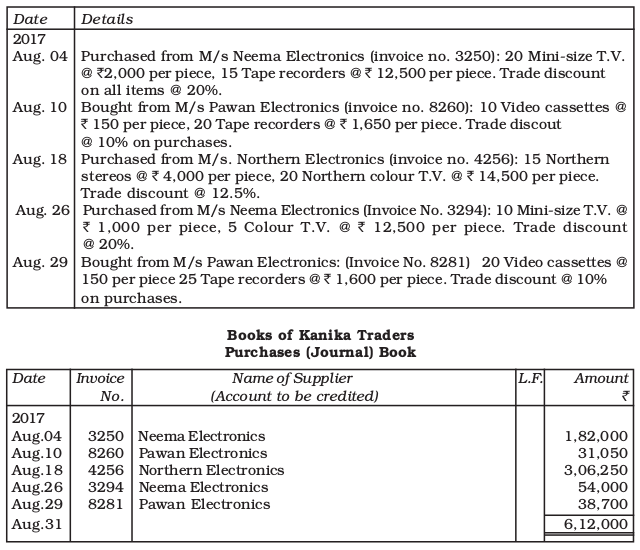

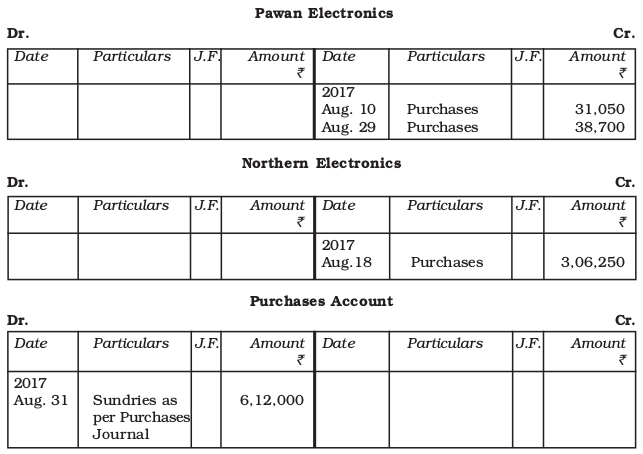

The monthly total of the purchases book is posted to the debit of purchases account in the ledger. Individual suppliers accounts may be posted daily. Consider the following details obtained from M/s Kanika Traders and observe how the entries are recorded in the purchase journal.

Posting from the purchases journal is done daily to their respective accounts with the relevant amounts on the credit side. The total of the purchases journal is per4.5 Sales Return (Journal) Book4.5 Sales Return (Journal) Bookiodically posted to the debit of the purchases account normally on the monthly basis. However, if the number of transactions is very large, this total may be done and posted at some other convenient time interval such as daily, weekly or fortnightly. The posting from the purchases journal to the ledger from is illustrated as follows:

Books of Kanika Electronics

Neema Electronics

| Date | Particulars | J.F. | Amount Rs. | Date | Particulars | J.F. | Amount Rs |

| 2017 Aug.04 Aug.26 | Purchases Purchases | 1,82,000 54,000 |

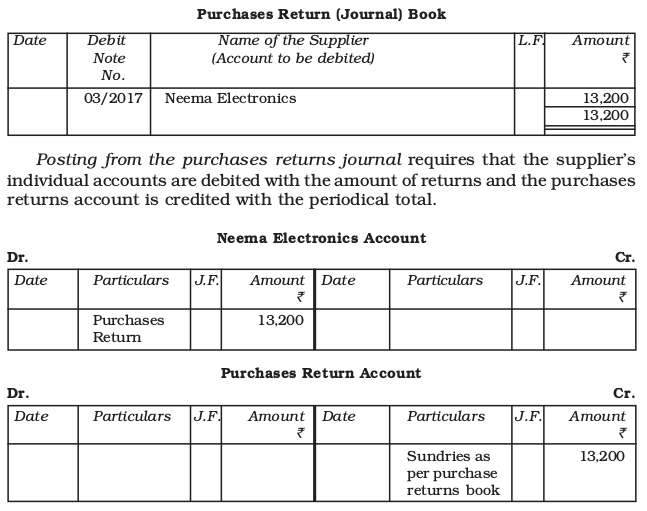

4.3 Purchases Return (Journal) Book

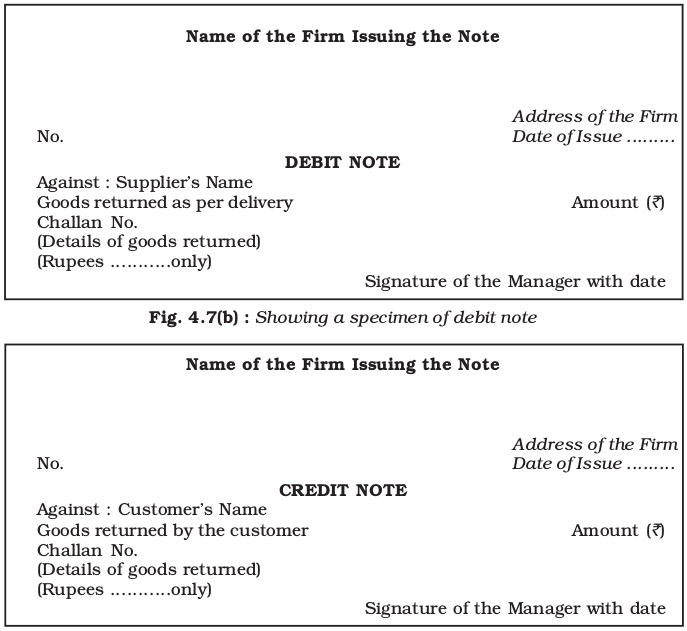

In this book, purchases return of goods are recorded. Sometimes goods purchased are returned to the supplier for various reasons such as the goods are not of the required quality, or are defective, etc. For every return, a debit note (in duplicate) is prepared and the original one is sent to the supplier for making necessary entries in his book. The supplier may also prepare a note, which is called the credit note. The source document for recording entries in the purchases return journal is generally a debit note. A debit note will contain the name of the party (to whom the goods have been returned) details of the goods returned and the reason for returning the goods. Each debit note is serially numbered and dated. The format of the purchases return journal is shown in figure 4.7(a).

Purchases Return (Journal) Book

| Date | debit Note No. | Name of Supplier (Account to be debited) | L.F. | Amount Rs. |

Fig 4.7(a) : Format of Purchases return (journal) book

Box 2

Debit and Credit Notes

A Debit note is a document evidencing a debit to be raised against a party for reasons other than sale on credit. On finding that goods supplied are not as per the terms of the order placed, the defective goods are returned to the supplier of the goods and a note is prepared to debit the supplier; or when an additional sum is recoverable from a customer such a note is prepared to debit the customer with the additional dues. In these two situations the note is called a debit note (refer figure 4.7(b)). A Credit note is prepared, when a party is to be given a credit for reasons other than credit purchase. It is a common practice to make it in red ink. When goods are received back from a customer, a credit note should be sent to him. The suggested proforma of credit note is shown in figure 4.7(c).

Fig. 4.7(c) : Showing a specimen credit note

Refer to the purchases (journal) book of Kanika Traders you will notice that 20 mini size T.V.’s and 15 tape- recorders were bought from Neema Electronics for ` 1,82,000 However, on delivery 2 mini T.V.’s and tape recorders were found defective and were returned back vide debit note no. 03/2017. In this case, the purchases return books will be prepared as follows :

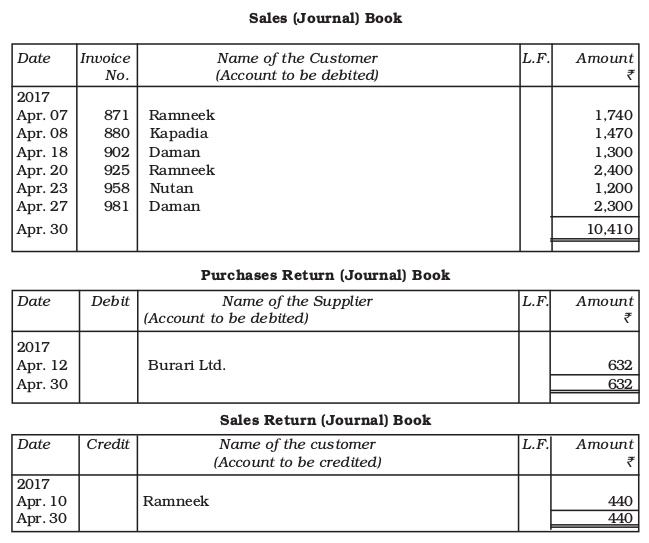

4.4 Sales (Journal) Book

All credit sales of merchandise are recorded in the sales journal. Cash sales are recorded in the cash book. The format of the sales journal is similar to that of the purchases journal explained earlier. The source document for recording entries in the sales journal are sales invoice or bill issued by the firm to the customers. The date of sale, invoice number, name of the customer and amount of the invoice are recorded in the sales journal. Other details about the sales transaction including terms of payment are available in the invoice. In fact, two or more than two copies of a sales invoice are prepared for each sale. The book keeper makes entries in the sales journal from one copy of the sales invoice. The format of the sales joournal is shown in figure 4.8. In the sales journal, one additional column may be added to record sales tax recovered from the customer and to be paid to the government within the stipulated time. Periodically, at the end of each month the amount column is total led and posted to the credit of sales account in the ledger. Posting to the debit side of individual customer’s accounts may be made daily.

Sales (Journal) Book

| Date | Invoice No. | Name of the Customer (Account to be debited) | L.F. | Amount Rs. |

Fig. 4.8 : Format of sales (journal) cash book

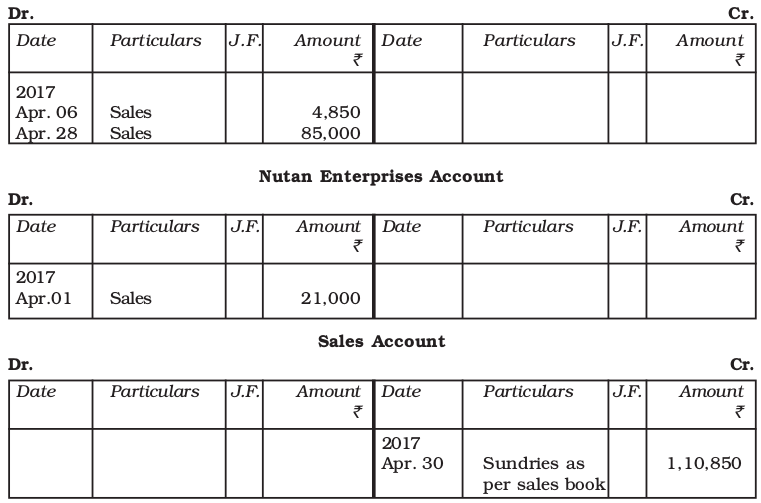

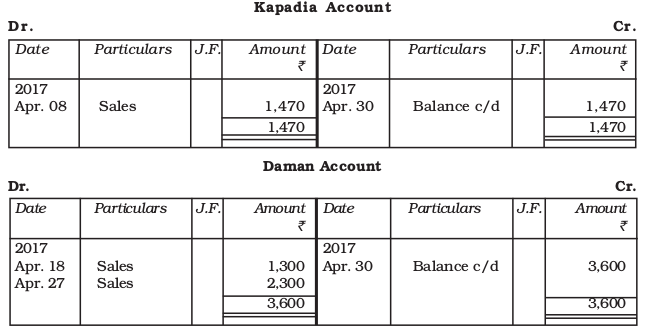

For example M/s Koina Supplies sold on credit:

(i) Two water purifiers @ ` 2,100 each and five buckets @ ` 130 each to M/s Raman Traders (Invoice no. 178 dated April 06, 2017).

(ii) Five road side containers @ ` 4,200 each to M/s Nutan enterprises (Invoice no 180 dated April 09, 2017) .

(iii) 100 big buckets @ ` 850 each to M/s Raman traders (Invoice no. 209, dated April 28, 2017).

The above stated transactions will be entered in a sales journal as follows:

Books of Koina Suppliers

Sales (Journal) Book

| Date...... | Invoice No. | Name of the Customer (Account to be debited) | L.F. | Amount Rs. |

| 2017 April 06 April 09 April 28 April 30 | 178 180 209 | Raman Traders Nutan Enterprises Raman Traders | 4,850 21,000 85,000 1,10,850 |

Posting from the sales journal are done to the debit of customer’s accounts kept in the ledger. Like the purchases journal, individual customer’s accounts are generally posted daily, with the amount involved. The sales journal is also totaled periodically (generally monthly), and this total is credited to sales account in the ledger. The sales (journal) book illustrated above will be posted in the related ledger account in the following manner:

Raman Traders Account

4.5 Sales Return (Journal) Book

This journal is used to record return of goods by customers to them on credit. On receipt of goods from the customer, a credit note is prepared, like the debit note referred to earlier. The difference between the credit not and the debit note is that the former is prepared by the seller and the latter is prepared by the buyer. Like the debit note, the credit note is also prepared in duplicate and contains detail relating to the name of the customer, details of the merchandise received back and the amount. Each credit note is serially numbered and dated. The source document for recording entries in the sales return book is generally the credit note. The format of the sales return book is shown in figure 4.9

Sales Return (Journal) Book

| Date | Credit No. | Name of the Customer (Account to be Credited) | L.F. | Amount Rs. |

Fig. 4.9 : Format of sales return (journal) book

Refer to the sales (journal) book of Koina Supplier of you will find that two water purifiers were sold to Raman Traders for ` 2,100 each, out of which one purifier was returned back due to the manufacturing defect (credit note no. 10/2017). In this case, the sales return (Journal) book will be prepared

as follows :

Sales Return (Journal) Book

| Date | Credit No. | Name of the Customer (Account to be Credited) | L.F. | Amount Rs. |

| 10/2017 | Raman Traders | 2,100 2,100 |

Posting to the sales return journal requires that the customer’s account be credited with the amount of returns and the sales return account be debited with the periodical total in the same way as is done in case of posting from the purchases journal.

Raman Traders Account

| Date | Particulars | J.F. | Amount Rs. | Date | Particulars | J.F. | Amount Rs |

| Sales Return | 2,100 |

| Date | Particulars | J.F. | Amount Rs. | Date | Particulars | J.F. | Amount Rs |

| Sundries as per sales return book | 2,100 |

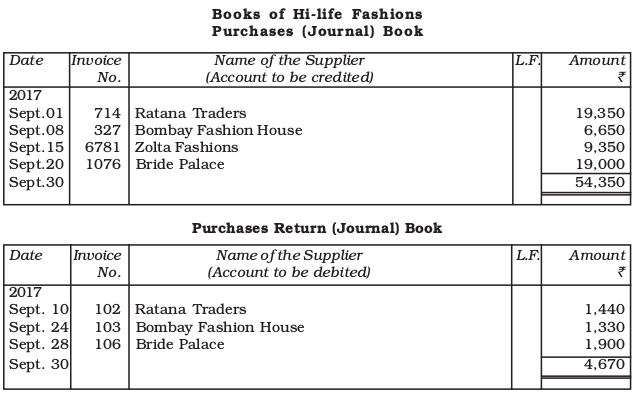

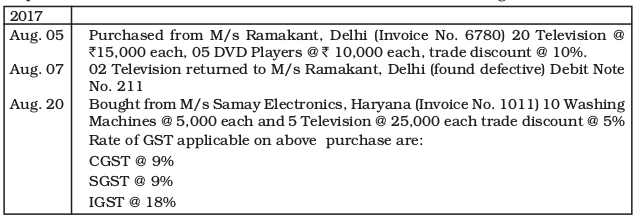

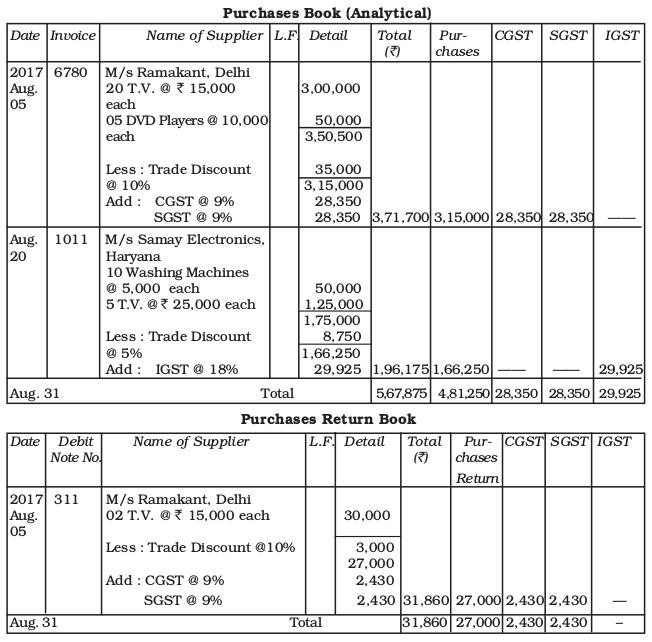

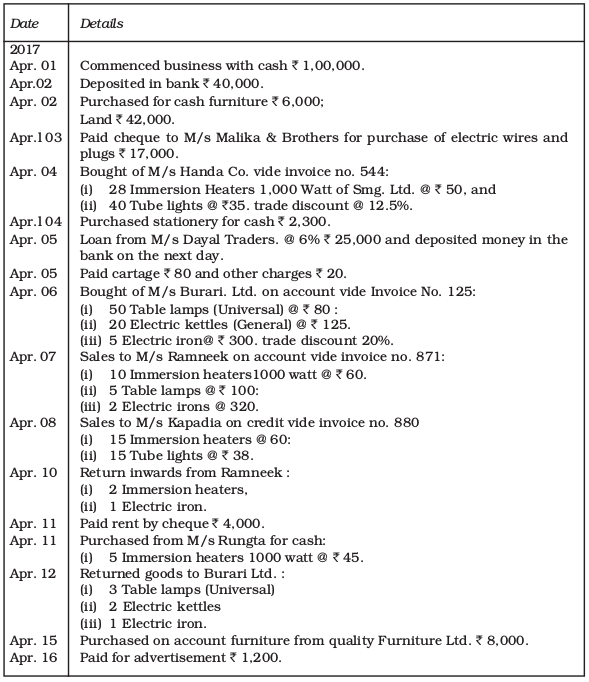

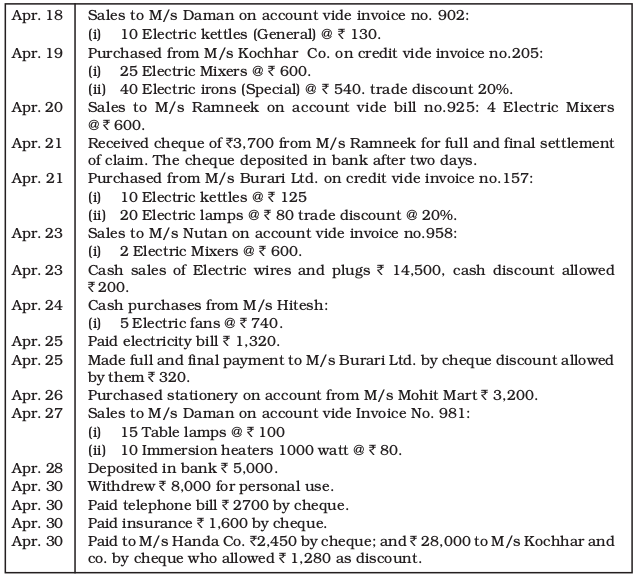

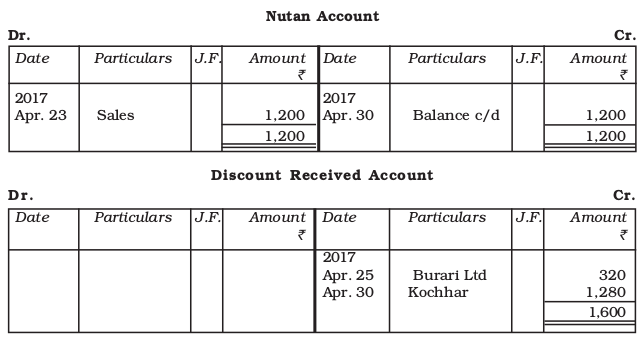

Enter the following transactions of M/s Hi-Life Fashions in purchases and purchases return book and post them to the ledger accounts for the month of September 2014:

| Date...... | Details |

| 2017 Sept. 01 Sept. 08 Sept. 10 Sept. 15 Sept. 20 Sept. 24 Sept. 28 | Purchase of following goods on credit from M/s Ratna Traders, as per Invoice No.714: 25 Shirts @ `300 per shirt 20 Pants @ `700 per pant Less 10% trade discount Purchase of following goods on credit from M/s Bombay Fashion House, as per Invoice No.327 ; 10 Fancy Trousers @ `500 per trouser 20 Fancy Hat @ ` 100 per hat Less 5% trade discount Goods returned to M/s Ratana Traders, as per debit note No.102 : 3 shirts @ `300 per shirt 1 Pant @ `700 per pant Less 10% trade discount Purchase of following goods on credit from M/s Zolta Fashions, as per Invoice No.6781 : 10 Jackets @ `1000 per jacket 5 Plain shirts `200 per shirts Less 15% trade discount. Purchase of following goods on credit from M/s Bride Palace, as per Invoice No.1076 : 10 Fancy Lengha @ `2,000 per lengha Less 5% trade discount. Goods returned to M/s Bombay Fashion House as per debit note No.103 : 2 Fancy Trousers @ `500 per trouser 4 Fancy Hat @ `100 per hat Less 5% trade discount. Goods returned to M/s Bride Palace as per debit note No.105 : 1 Fancy Lengha @ `2,000 per lengha Less 5% trade discount. |

Solution

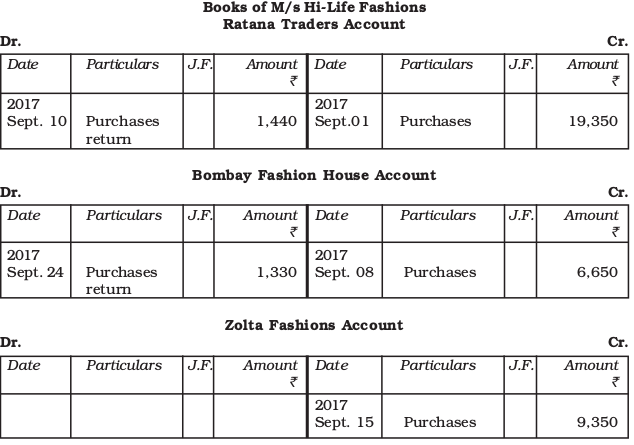

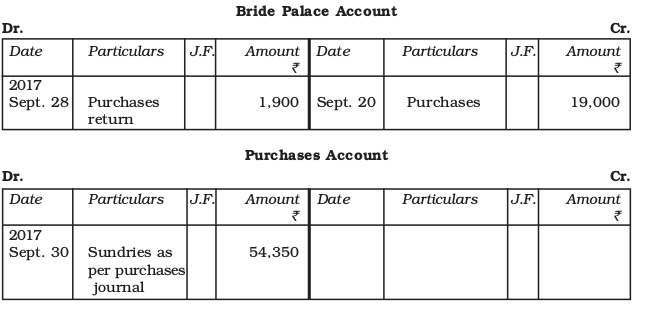

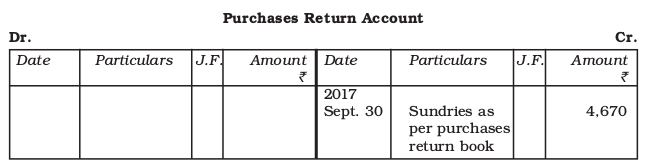

(ii) Ledger Posting

Recording of Transactions - II

Illustration 6

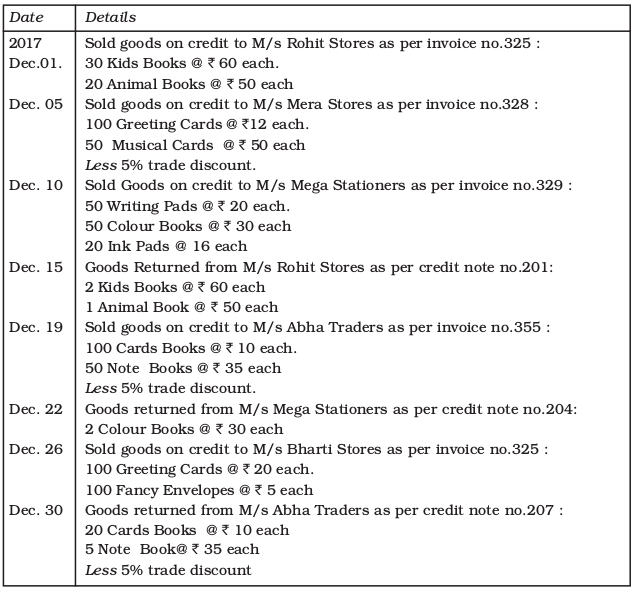

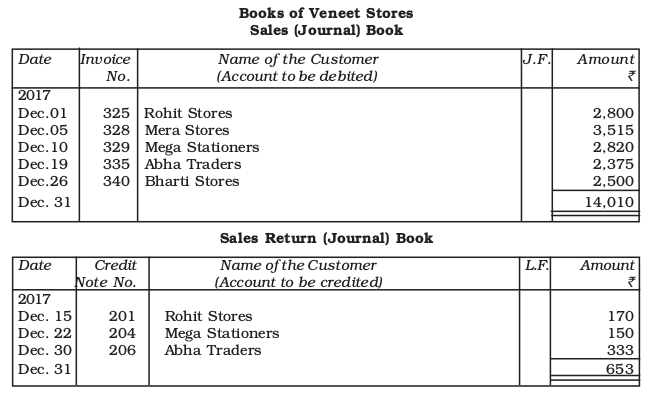

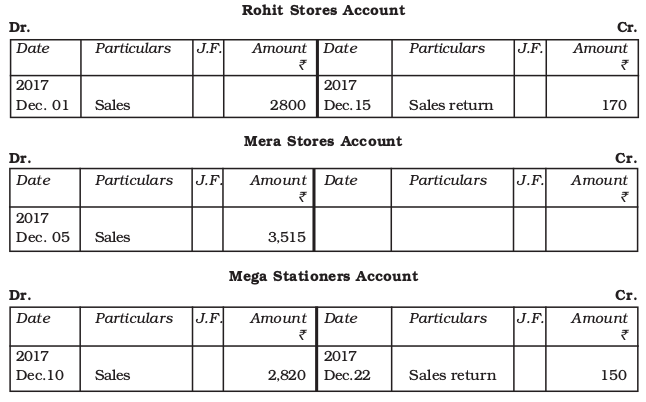

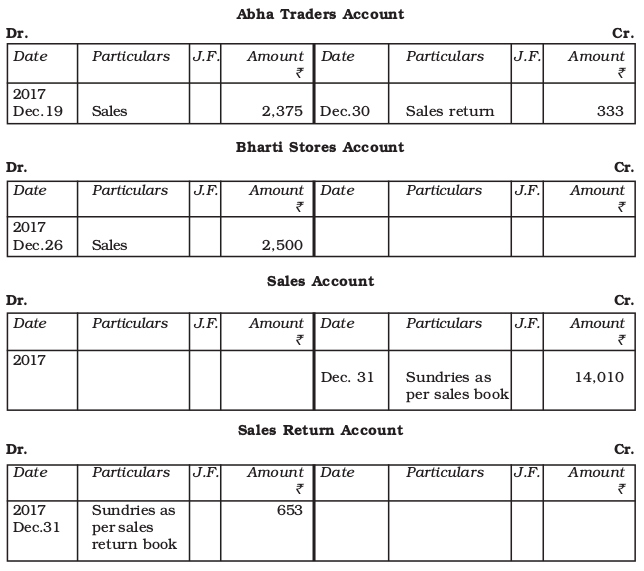

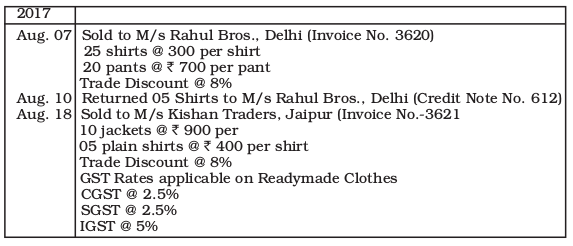

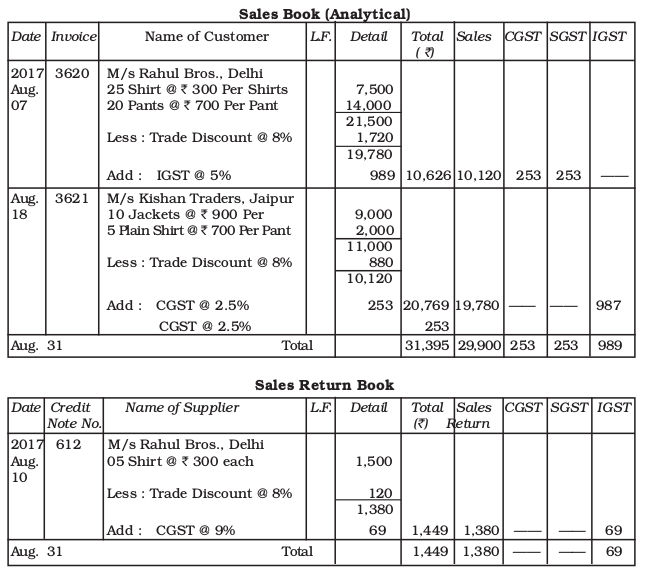

Enter the following transactions in the Sales and Sales Return book of M/s Vineet Stores:

Solution

(ii) Ledger Posting

Recording of Transactions - II

Illustration: 7

Prepare Purchases book and Purchases Return Book firm the following transactions:

Illustration : 8

Prepare Sales book and Sales Return Book of M/s Akash of Rajasthan from the following

transactions :

Recording of Transactions - II

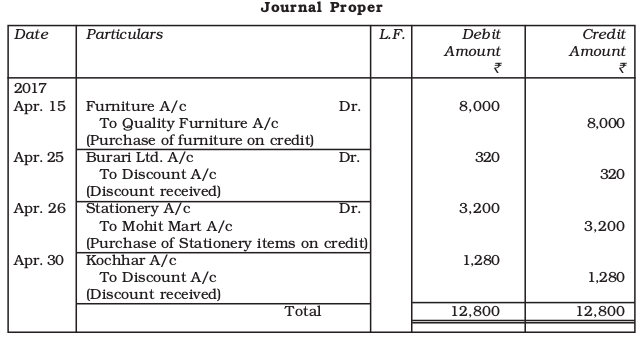

4.6 Journal Proper

A book maintained to record transactions, which do not find place in special journals, is known as Journal Proper or Journal Residual.

Following transactions are recorded in this journal:

1. Opening Entry: In order to open new set of books in the beginning of new accounting year and record therein opening balances of assets, liabilities and capital, the opening entry is made in the journal.

2. Adjustment Entries: In order to update ledger account on accrual basis, such entries are made at the end of the accounting period. Such as Rent outstanding, Prepaid insurance, Depreciation and Commission received in advance.

3. Rectification entries: To rectify errors in recording transactions in the books of original entry and their posting to ledger accounts this journal is used.

4. Transfer entries: Drawing account is transferred to capital account at the end of the accounting year. Expenses accounts and revenue accounts which are not balanced at the time of balancing are opened to record specific transactions. Accounts relating to operation of business such as Sales, Purchases, Opening Stock, Income, Gains and Expenses, etc., and drawing are closed at the end of the year and their Total/balances are transferred to Trading and Profit and Loss account by recording the journal entries. These are also called closing entries.

5. Other entries: In addition to the above mentioned entries in the points number 1 to 4, recording of the following transaction is done in the journal proper :

(i) At the time of a dishonour of a cheque the entry for cancellation for discount received or discount allowed earlier.

(ii) Purchase/sale of items on credit other than goods.

(iii) Goods withdrawn by the owner for personal use.

(iv) Goods distributed as samples for sales promotion.

(v) Endorsement and dishonour of bills of exchange.

(vi) Transaction in respect of consignment and joint venture, etc.

(vii) Loss of goods by fire/theft/spoilage.

Test Your Understanding - I

Select the Correct Answer

(a) When a firm maintains a cash book, it need not maintain ;

(i) Journal Proper

(ii) Purchases (journal) book

(iii) Sales (journal) book

(iv) Bank and cash account in the ledger

(b) Double column cash book records:

(i) All transactions

(ii) Cash and bank transactions

(iii) Only cash transactions

(iv) Only credit transactions

(c) Goods purchased on cash are recorded in the :

(i) Purchases (journal) book

(ii) Sales (journal) book

(iii) Cash book

(iv) Purchases return (journal) book

(d) Cash book does not record transaction of :

(i) Cash nature

(ii) Credit nature

(iii) Cash and credit nature

(iv) None of these

(e) Total of these transactions is posted in purchase account :

(i) Purchase of furniture

(ii) Cash and credit purchase

(iii) Purchases return

(iv) Purchase of stationery

(f) The periodic total of sales return journal is posted to :

(i) Sales account

(ii) Goods account

(iii) Purchases return account

(iv) Sales return account

(g) Credit balance of bank account in cash book shows :

(i) Overdraft

(ii) Cash deposited in our bank

(iii) Cash withdrawn from bank

(iv) None of these

(h) The periodic total of purchases return journal is posted to :

(i) Purchase account

(ii) Profit and loss account

(iii) Purchase returns account

(iv) Furniture account

(i) Balancing of account means :

(i) Total of debit side

(ii) Total of credit side

(iii) Difference in total of debit & credit

(iv) None of these

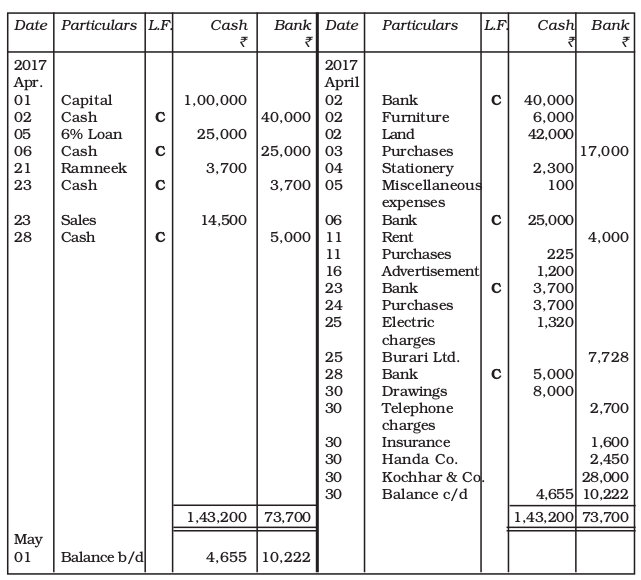

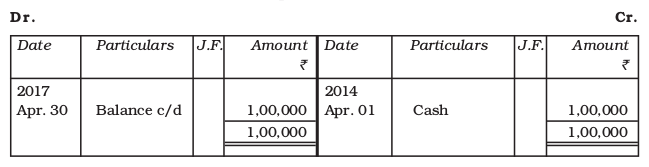

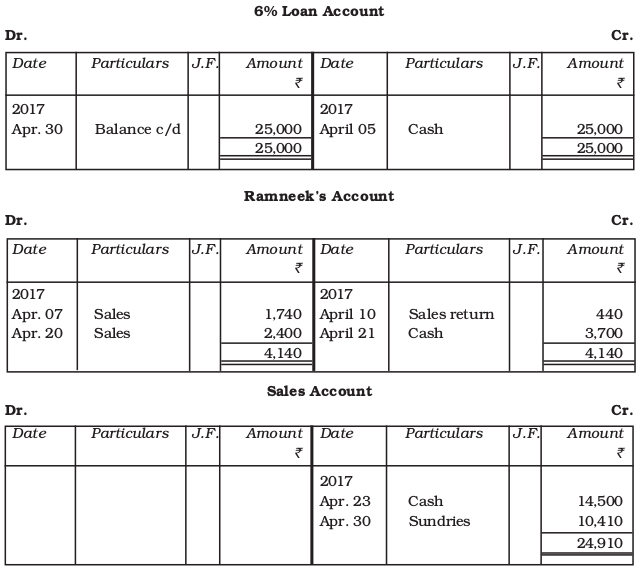

4.7 Balancing the Accounts

Accounts in the ledger are periodically balanced, generally at the end of the accounting period, with the object of ascertaining the net position of each amount. Balancing of an account means that the two sides are totaled and the difference between them is shown on the side, which is shorter in order to make their totals equal. The words ‘balance c/d’ are written against the amount of the difference between the two sides. The amount of balance is brought (b/d) down in the next accounting period indicating that it is a continuing account, till finally settled or closed.

In case the debit side exceeds the credit side, the difference is written on the credit side, if the credit side exceeds the debit side, the difference between the two appears on the debit side and is called debit and credit balance respectively. The accounts of expenses losses and gains/revenues are not balanced but are closed by transferring to trading and profit and loss account. The balancing of the an account is illustrated below with the help of an example explaining the complete process of recording the transactions, posting to ledger and balancing there of.

Cash Book

The recorded transactions will be posted in the ledger.

Test Your Understanding - II

1. Fill in the Correct Words :

(a) Cash book is a ......... journal.

(b) In Journal proper, only.........discount is recorded.

(c) Return of goods purchased on credit to the suppliers will be entered in ...... Journal.

(d) Assets sold on credit are entered in .........

(e) Double column cash book records transaction relating to .........and .........

(f) Total of the debit side of cash book is .........than the credit side.

(g) Cash book does not record the .........transactions.

(h) In double column cash book .........transactions are also recorded.

(i) Credit balance shown by a bank column in cash book is .........

(j) The amount paid to the petty cashier at the beginning of a period is known as .........amount.

(k) In purchase book goods purchased on .........are recorded.

2. State whether the following statements are True or False :

(a) Journal is a book of secondary entry.

(b) One debit account and more than one credit account in a entry is called compound entry.

(c) Assets sold on credit are entered in sales journal.

(d) Cash and credit purchases are entered in purchasejJournal.

(e) Cash sales are entered in sales journal.

(f) Cash book records transactions relating to receipts and payments.

(g) Ledger is a subsidiary book.

(h) Petty cash book is a book having record of big payments.

(i) Cash received is entered on the debit side of cash book.

(j) Transaction recorded both on debit and credit side of cash book is known as contra entry.

(k) Balancing of account means total of debit and credit side.

(l) Credit purchase of machine is entered in purchase journal.

Key Terms Introduced in the Chapter

• Posting • Sales (Journal) Book

• Day books • Balancing of Accounts

• Cash book • Purchase (Journal) book

• Petty Cash book • Purchases return (Journal) Book

• Sales return (Journal) Book

Summary with Reference to Learning Objectives

1. Journal : Basic book of original entry.

2. Cash book : A book used to record all cash receipts and payments.

3. Petty cash book : A book used to record small cash payments.

4. Purchase journal : A special journal in which only credit purchases are recorded

5. Sales journal : A special journal in which only credit sales are recorded

6. Purchases Return Book : A book in which return of merchandise purchased is recorded.

7. Sales Return Book : A special book in which returns of merchandise sold on credit are recorded.

Questions For Practice

Short Answers

1. Briefly state how the cash book is both journal and a ledger.

2. What is the purpose of contra entry?

3. What are special purpose books?

4. What is petty cash book? How it is prepared?

5. Explain the meaning of posting of journal entries?

6. Define the purpose of maintaining subsidiary journal.

7. Write the difference between return Inwards and return ouwards.

8. What do you understand by ledger folio?

9. What is difference between trade discount and cash discount?

10. Write the process of preparing ledger from a journal.

11. What do you understand by Imprest amount in petty cash book?

Long Answers

1. Explain the need for drawing up the special purpose books.

2. What is cash book? Explain the types of cash book.

3. What is contra entry? How can you deal this entry while preparing double column cash book?

4. What is petty cash book? Write the advantages of petty cash book?

5. Describe the advantages of sub-dividing the Journal.

6. What do you understand by balancing of account?

Numerical Questions

Simple Cash Book

1. Enter the following transactions in a simple cash book for December 2016:

01 Cash in hand -₹12,000

05 Cash received from Bhanu -₹ 4,000

07 Rent Paid -₹2,000

10 Purchased goods Murari for cash -₹ 6,000

15 Sold goods for cash -₹ 9,000

18 Purchase stationery -₹300

22 Cash paid to Rahul on account -₹ 2,000

28 Paid salary -₹ 1,000

30 Paid rent -₹500

(Ans. Cash in hand -₹13,200)

2. Record the following transaction in simple cash book for November 2016:

01 Cash in hand -₹12,500

04 Cash paid to Hari -₹600

07 Purchased goods -₹800

12 Cash received from Amit -₹1,960

16 Sold goods for cash -₹800

20 Paid to Manish -₹590

25 Paid cartage -₹100

31 Paid salary -₹1,000

(Ans. Cash in hand -₹ 12,170)

3. Enter the following transaction in Simple cash book for December 2017:

01 Cash in hand -₹7,750

06 Paid to Sonu -₹45

08 Purchased goods -₹600

15 Received cash from Parkash -₹960

20 Cash sales -₹ 500

25 Paid to S.Kumar -₹1,200

30 Paid rent -₹600

(Ans. Cash in hand -₹6,765)

Bank Column Cash Book

4. Record the following transactions in a bank column cash book for December 2016:

01 Started business with cash -₹80,000

04 Deposited in bank -₹50,000

10 Received cash from Rahul -₹1,000

15 Bought goods for cash -₹8,000

22 Bought goods by cheque -₹10,000

25 Paid to Shyam by cash -₹20,000

30 Drew from Bank for office use -₹2,000

31 Rent paid by cheque -₹1,000

(Ans. Cash in hand -₹ 5,000: cash at bank -₹ 37,000)

5. Prepare a double column cash book with the help of following information for December 2016:

01 Started business with cash -₹1,20,000

03 Cash paid into bank -₹50,000

05 Purchased goods from Sushmita -₹20,000

06 Sold goods to Dinker and received a cheque -₹ 20,000

10 Paid to Sushmita cash -₹20,000

14 Cheque received on December 06, 2016 deposited into bank

18 Sold goods to Rani -₹12,000

20 Cartage paid in cash -₹500

22 Received cash from Rani -₹12,000

27 Commission received -₹5,000

30 Drew cash for personal use -₹2,000

(Ans. Cash in hand ` 64,500 : Cash at bank -₹70,000)

6. Enter the following transactions in double column cash book of M/s Ambica Traders for July 2017:

01 Commenced business with cash -₹50,000

03 Opened bank account with ICICI -₹30,000

05 Purchased goods for cash -₹10,000

10 Purchased office machine for cash -₹5,000

15 Sales goods on credit from Rohan and received chaeque -₹7,000

18 Cash sales -₹8,000

20 Rohan’s cheque deposited into bank 22 Paid cartage by cheque -₹500

25 Cash withdrawn for personal use -₹2,000

30 Paid rent by cheque -₹ 1,000

(Ans. Cash in hand -₹11,000, Cash at bank -₹35,500)

7. Prepare double column cash book from the following information for

July 2017:

01 Cash In hand -₹7,500

Bank overdraft -₹3,500

03 Paid wages -₹200

05 Cash sales -₹7,000

10 Cash deposited into bank -₹4,000

15 Goods purchased and paid by cheque -₹2,000

20 Paid rent -₹500

25 Drew from bank for personal use -₹400

30 Salary paid 1,000 (Ans. Cash in hand ` 8,800, Bank overdraft -₹ 1,900)

8. Enter the following transaction in a double column cash book of M/s.Mohit Traders for January 2017:

01 Cash in hand -₹3,500

Bank overdraft -₹2,300

03 Goods purchased for cash -₹1,200

05 Paid wages -₹200

10 Cash sales -₹8,000

15 Deposited into bank -₹6,000

22 Sold goods for cheque which was deposited into -₹2,000

bank same day

25 Paid rent by cheque -₹1,200

28 Drew from bank for personal use -₹1,000

31 Bought goods by cheque -₹1,000

(Ans. Cash in hand -₹4,100 Cash at bank -₹2,500)

9. Prepare double column cash book from the following transactions for the year August 2017:

01 Cash in hand -₹17,500

Cash at bank -₹5,000

03 Purchased goods for cash -₹3,000

05 Received cheque from Jasmeet -₹10,000

08 Sold goods for cash -₹7,000

10 Jasmeet’s cheque deposited into bank

12 Purchased goods and paid by cheque -₹20,000

15 Paid establishment expenses through bank -₹1,000

18 Cash sales -₹7,000

20 Deposited into bank -₹10,000

24 Paid trade expenses -₹500

27 Received commission by cheque -₹ 6,000

29 Paid Rent -₹2,000

30 Withdrew cash for personal use -₹1,200

31 Salary paid -₹6,000

(Ans. Cash in hand -₹8,800 cash at bank -₹10,000)

10. M/s Ruchi trader started their cash book with the following balances on July 2017: cash in hand -₹1,354 and balance in bank current account -₹7,560. He had the following transaction in the month of July 2017:

03 Cash sales -₹2,300

05 Purchased goods, paid by cheque -₹6,000

08 Cash sales -₹10,000

12 Paid trade expenses -₹700

15 Sales goods, received cheque (deposited same day) -₹20,000

18 Purchased motor car paid by cheque -₹15,000

20 Cheque received from Manisha (deposited same day) -₹10,000

22 Cash Sales -₹7,000

25 Manisha’s cheque returned dishonoured

28 Paid Rent -₹2,000

29 Paid telephone expenses by cheque -₹500

31 Cash withdrawn for personal use 2,000 Prepare bank column cash book

(Ans. Cash in hand -₹15,954 cash at bank -₹6,060)

Petty Cash Book

11. Prepare petty cash book from the following transactions. The imprest amount is -₹2,000.

2017

January

01 Paid cartage -₹50

02 STD charges -₹40

02 Bus fare -₹20

03 Postage -₹30

04 Refreshment for employees -₹80

06 Courier charges -₹30

08 Refreshment of customer -₹50

10 Cartage 35 15 Taxi fare to manager -₹70

18 Stationery -₹65

20 Bus fare -₹10

22 Fax charges -₹30

25 Telegrams charges -₹35

27 Postage stamps -₹200

29 Repair on furniture -₹105

30 Laundry expenses -₹115

31 Miscellaneous expenses -₹100

(Ans. Cash balance -₹935)

12. Record the following transactions during the week ending Dec.30, 2014 with a weekly imprest -₹ 500.

2017

January

24 Stationery -₹ 100

25 Bus fare -₹12

25 Cartage -₹40

26 Taxi fare -₹80

27 Wages to casual labour -₹90

29 Postage -₹80

(Ans. Cash balance -₹98)

Other Subsidiary Books

13. Enter the following transactions in the Purchase Journal (Book) of

M/s Gupta Traders of July 2017:

01 Bought from Rahul Traders as per invoice no.20041

40 Registers @ ₹60 each

80 Gel Pens @ ₹15 each

50 note books @ ₹20 each

Trade discount 10%.

15 Bought from Global Stationers as per invoice no.1132

40 Ink Pads @ ₹8 each

50 Files @ ₹10 each

20 Color Books @ ₹20 each

Trade Discount 5%

23 Purchased from Lamba Furniture as per invoice no. 3201

2 Chairs @ ₹600 per chair

1 Table @ ₹1000 per table

25 Bought from Mumbai Traders as per invoice no.1111

10 Paper Rim @ ₹100 per rim

400 drawing Sheets @ ₹3 each

20 Packets waters colour @ ₹40 per packet

(Ans: Total of purchases book ₹ 8,299)

14. Enter the following transactions in sales (journal) book of M/s.Bansal electronics:

2014

September

01 Sold to Amit Traders as per bill no.4321

20 Pocket Radio @ 70 per Radio

2, T.V. set, B&W.(6”) @ 800 Per T.V.

10. Sold to Arun Electronics as per bill no.4351

5 T.V. sets (20”) B&W @ ₹3,000 per T.V.

2 T.V. sets (21”) Colour @ ₹4,800 per T.V.

22 Sold to Handa Electronics as per bill no.4,399

10 Tape recorders @ ₹600 each

5 Walkman @ ₹ 300 each

28 Sold to Harish Trader as per bill no.4430

10 Mixer Juicer Grinder @ ₹ 800 each.

(Ans. Total of sales book ₹ 43,100)

15. Prepare a purchases return (journal) book from the following transactions for April 2017.

2017

April

05 Returned goods to M/s Kartik Traders 1,200

10 Goods returned to Sahil Pvt. Ltd. 2,500

17 Goods returned to M/s Kohinoor Traders.

for list price ₹2,000 less 10% trade discount.

28 Return outwards to M/s Handa Traders 550

(Ans. Total of purchases return book ₹ 6,150)

16. Prepare Return Inward Journal (Book) from the following transactions of

M/s Bansal Electronics for July 2017:

2017 `

July

04 M/s Gupta Traders returned the goods 1,500

10 Goods returned from M/s Harish Traders 800

18 M/s Rahul Traders returned the goods not as per 1,200

specifications

28 Goods returned from Sushil Traders 1,000

(Ans : Total of sales return ₹4,500)

Recording, Posting and Balancing

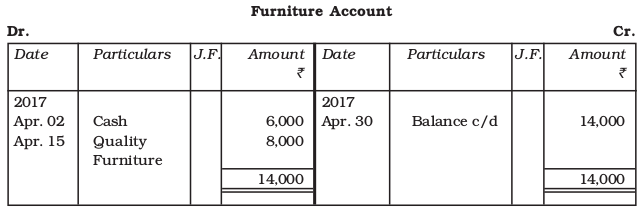

17. Prepare proper subsidiary books and post them to the ledger from the following transactions for the month of February 2017:

2017

February

01 Goods sold to Sachin 5,000

04 Purchase from Kushal Traders 2,480

06 Sold goods to Manish Traders 2,100

07 Sachin returned goods 600

08 Returns to Kushal Traders 280

10 Sold to Mukesh 3,300

14 Purchased from Kunal Traders 5,200

15 Furniture purchased from Tarun 3,200

17 Bought of Naresh 4,060

20 Return to Kunal Traders 200

22 Return inwards from Mukesh 250

24 Purchased goods from Kirit & Co. for list price of 5,700

less 10% trade discount

25 Sold to Shri Chand goods 6600

less 5% trade discount

26 Sold to Ramesh Brothers 4,000

28 Return outwards to Kirit and Co. 1,000

less 10% trade discount

28 Ramesh Brothers returned goods ₹500.

Ans : (Total of sales book `20,670, purchases book ₹16,870,

Purchases return book ₹1,380, sales return book ₹1,350).

18. The following balances of ledger of M/s Marble Traders on April 01, 2017

2017

April

Cash in hand -₹6,000

Cash at bank -₹12,000

Bills receivable -₹7,000

Ramesh (Cr.) -₹3,000

Stock (Goods) -₹5,400

Bills payable -₹2,000

Rahul (Dr.) -₹9,700

Himanshu (Dr.) -₹10,000

Transactions during the month were:

April

01 Goods sold to Manish -₹3,000

02 Purchased goods from Ramesh -₹8,000

03 Received cash from Rahul in full settlement -₹9,200

05 Cash received from Himanshu on account -₹4,000

06 paid to Remesh by cheque -₹6,000.

08 Rent paid by cheque -₹1,200

10 Cash received from manish -₹3,000

12 Cash sales -₹6,000

14 Goods returned to Ramesh -₹1,000

15 Cash paid to Ramesh in full settlement -₹3,700

Discount received -₹300

18 Goods sold to Kushal-₹10,000

20 Paid trade expenses -₹200

21 Drew for personal use -₹1,000

22 Goods return from Kushal -₹1,200

24 Cash received from Kushal -₹6,000

26 Paid for stationery -₹100

27 Postage charges -₹60

28 Salary Paid -₹2,500

29 Goods purchased from Sheetal Traders -₹7,000

30 Sold goods to Kirit -₹6000

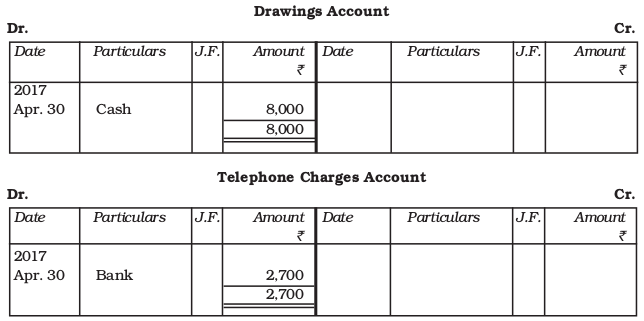

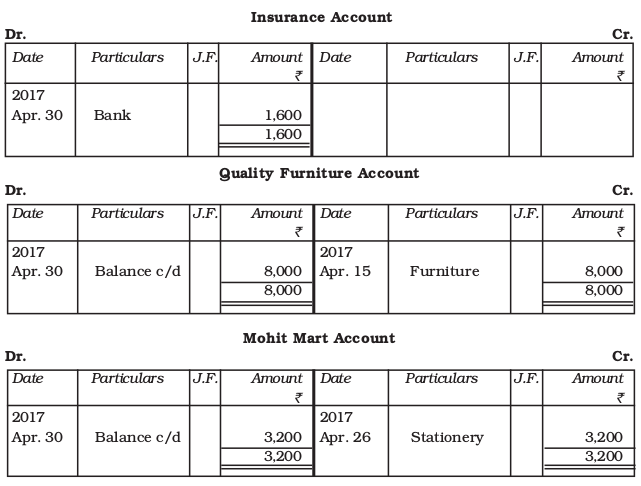

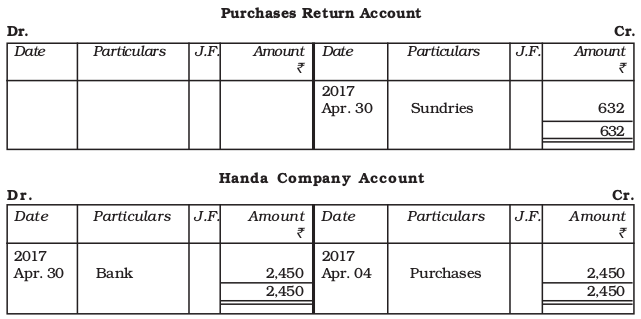

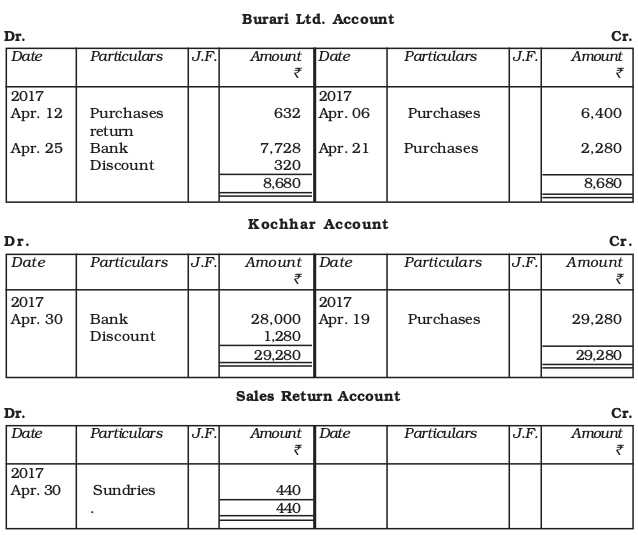

Goods purchased from Handa Traders -₹5,000

Journlise the above transactions and post them to the ledger.

Checklist to Test Your Understanding

Test Your Understanding - I

a. (iv) b. (ii) c. (iii) d. (ii) e. (ii) f. (iv) g .(ii) h. (iii) i. (iii)

Test Your Understanding - II

1. (a) subsidiary (b) cash (c) purchases return (d) journal proper

(e) cash, bank (f) more (g) credit (h) bank

(i) overdraft (j) imprest (k) credit

2. (a) False (b) True (c) False (d) False

(e) False (f) True (g) True (h) False

(i) True (j) True (k) False (l) False